What Jumbo Mortgage Rates Mean for Needham Buyers in 2026

If you’re buying or selling a home in Needham, MA, what do today’s jumbo mortgage rates actually mean for your transaction?

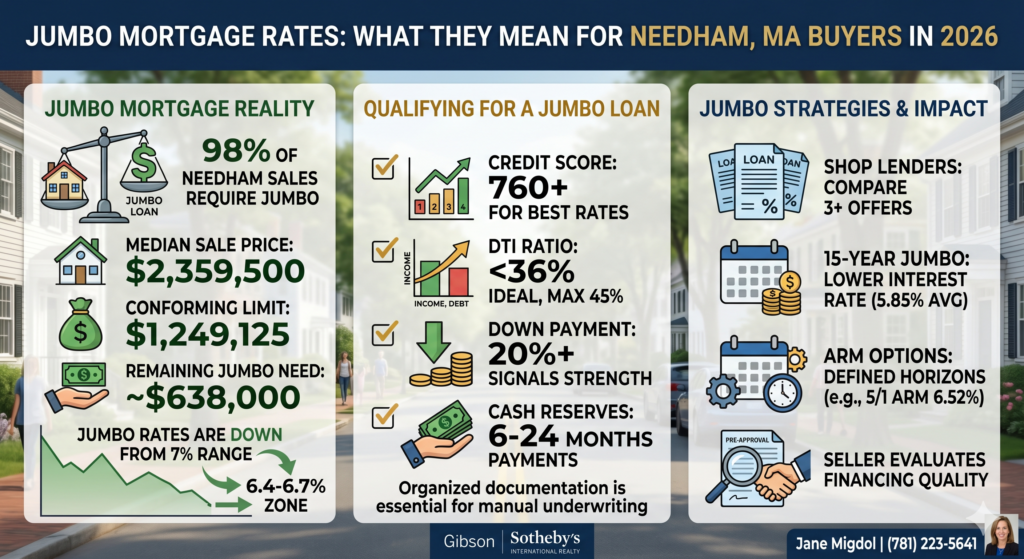

[SNIPPET ANSWER: With Needham’s 2026 median sale price at $2.36M and the conforming loan limit at $1,249,125, nearly every single-family purchase requires jumbo financing. Current 30-year jumbo rates average around 6.4% to 6.70% APR, down from 7% ranges seen in prior years.]

Why Jumbo Rates Matter for Every Needham Real Estate Transaction Right Now

I have been selling homes in Needham for 26 years, and here is something I tell every client before we discuss anything else: almost every single-family transaction in this town is a jumbo loan transaction. That is not an exaggeration. The 2026 year-to-date median single-family sale price in Needham is $2,359,500. Norfolk County’s conforming loan limit for 2026 sits at $1,249,125. Even if you put 20% down on a median-priced home, you need a mortgage of approximately $1,887,600, which is roughly $638,000 above the conforming threshold.

So whether you are the buyer arranging financing or the seller evaluating an offer, jumbo rates are not some abstract number. They shape what buyers can afford, how fast deals close, and ultimately what your Needham home sells for. With over 180 closed transactions and 130 five-star client reviews behind me, I can say with confidence that the financing conversation is where every successful Needham deal begins.

Where Needham Jumbo Rates Stand Right Now

You are going to hear a lot of different numbers depending on where you look, so let me simplify this for you. As of early June 2026, the national averages for jumbo mortgage products look like this:

- 30-Year Fixed Jumbo: approximately 6.40% to 6.70% APR depending on the source

- 15-Year Fixed Jumbo: approximately 5.85% APR

- 5/1 ARM Jumbo: approximately 6.52% APR

What is the big headline? Rates have come down meaningfully from the 7% range that dominated much of 2023 and 2024. That roughly 44-basis-point drop from a year ago does not sound dramatic, but on a $1.9M mortgage, the difference in your monthly payment is real.

Here is what makes this moment interesting for the MetroWest Boston real estate market: jumbo rates are currently running very close to, and in some cases slightly below, conventional conforming rates for strong borrowers. If you have a 720-plus credit score and 20% or more for a down payment, you may actually find yourself in a favorable rate tier. This is not the norm historically, and it will not last forever.

One couple I recently worked with had been watching Needham Heights homes for over a year, waiting for a “better rate environment.” When I showed them the numbers in spring 2026 compared to what they had been tracking, they realized the window had already opened. They locked a 30-year jumbo at a rate that put their monthly payment nearly $600 below where it would have been in late 2023. They closed on a turnkey Colonial within walking distance of the Needham Heights commuter rail stop on Chestnut Street.

How to Qualify for a Jumbo Loan in Needham, MA

The qualification bar for a jumbo mortgage is genuinely higher than what you see on the conforming side, and this is where I see buyers stumble most often. Here is what lenders are looking at:

Credit score: 700 minimum, though a score of 760 or above will unlock the most favorable jumbo rate tiers. For super-jumbo loans above $2M (common in neighborhoods like Birds Hill and along Gould Street near Needham Center), lenders typically want 720 to 740.

Debt-to-income ratio (DTI): No higher than 45%, and you will get better terms if you keep it below 36%. This means your total monthly debts, including projected housing costs, should not exceed 45% of your gross monthly income.

Down payment: 10% is the floor for most jumbo lenders, but 20% or more changes the game. It unlocks better rate tiers and signals financial strength to sellers in a multiple-offer situation, which is a meaningful edge in Needham’s competitive landscape.

Cash reserves: Expect lenders to verify 6 to 24 months of mortgage payments sitting in accessible accounts. Unlike conforming loans, where the process is heavily automated, jumbo loans involve manual underwriting. Every file gets a close look.

What I tell my clients is this: getting your financial house in order before you start touring is not optional in a market where 58% of Needham homes sell within 30 days. Arriving without a jumbo pre-approval is a disqualifying move. Many sellers at this price point expect to see it before they even accept a showing.

Why Needham Sellers Should Understand Their Buyer’s Financing

If you are on the selling side, you might be wondering why any of this matters to you. It matters because your buyer’s cost of capital directly affects what they can offer.

Consider this: Needham’s median single-family sale price is up 62% in four years. The average residential single-family assessed value increased by 22.28% to $1,464,398, and actual market prices consistently run 15 to 20 percent above assessments. When you list a home near Needham Center on Great Plain Avenue or in the Heights along Highland Avenue, you are selling into a market where every competitive buyer needs jumbo financing that takes longer to underwrite and involves stricter appraisal standards.

I recently helped a seller in Needham Center who received three offers on the first weekend. Two came with jumbo pre-approvals from well-known local lenders who had closed deals in town before. The third offer was slightly higher in price but came from a buyer whose lender had never closed a jumbo in Norfolk County. We went with one of the other two offers, and the deal closed in 35 days without a single hiccup. The lesson? A seller’s best Realtor in Needham will evaluate not just the offer price but the quality of the buyer’s financing.

Smart Jumbo Strategies That Give You an Edge in MetroWest Boston

Shopping lenders matters far more on jumbo loans than on conforming loans. Rates, qualification thresholds, and reserve requirements can vary significantly from lender to lender. I always encourage clients to talk to at least three lenders before committing. Here is what else you should consider:

The 15-Year Jumbo Conversation in Needham

At roughly 5.85% APR, the 15-year fixed jumbo rate is meaningfully lower than the 30-year rate. For buyers with strong cash flow who plan to stay in Needham long-term (and most do, given the school system rated 9 out of 10 by GreatSchools, the commuter rail access, and the community fabric), the interest savings over the life of the loan are substantial. This product makes particular sense if you are a move-up buyer already sitting on significant equity from a prior sale.

When an ARM Makes Sense

The introductory rate on a five-year ARM averaged around 6.27% in May 2026. For buyers with a defined time horizon, perhaps a corporate relocation with a 5-to-7-year window, an ARM can be the right financial tool. I have seen several biotech and tech professionals relocating to the Route 128 corridor use this strategy effectively.

Down Payment as a Competitive Tool

In a market where well-positioned homes in Needham Heights command $575 to $625 per square foot and sometimes sell in under two weeks, your down payment is not just about rate. It is about signaling seriousness. Putting 20 to 25% down versus the minimum 10% tells a seller you are financially strong, reducing their risk, especially when multiple offers are on the table.

Needham Neighborhoods and the Jumbo Financing Reality

Your financing picture looks different depending on where in Needham you are buying. Here is what I see on the ground:

Needham Heights: Turnkey new construction near the commuter rail stop on Chestnut Street regularly trades at $2.5M and above. You are deep into jumbo territory, and speed of closing matters to sellers who know demand is high.

Needham Center: Single-family homes within a few blocks of Great Plain Avenue range from $1.8M to $3.2M. Larger lots on Gould Street and West Street can trade above $3.5M. These are transactions where your lender’s experience with high-value appraisals is critical.

Birds Hill: Some of Needham’s premier homes sit here, with individual sales reaching $3.025M in 2026. Volume is low but prices are high, and your jumbo lender needs to be comfortable with estate-caliber valuations.

What ties all of these neighborhoods together is that a good lender is part of your team, not just a box to check. In my experience, buyers who close successfully in Needham have a lender who is responsive, who is local, and who has done jumbo transactions in this specific market before.

Frequently Asked Questions About Jumbo Loans in Needham, MA

What is the conforming loan limit in Needham for 2026?

Norfolk County, where Needham is located, has a 2026 conforming loan limit of $1,249,125 for single-family homes. Any mortgage above that threshold is classified as a jumbo loan. With Needham’s median sale price at $2,359,500, most transactions here exceed that limit significantly.

What credit score do I need for a jumbo loan in Needham?

Most lenders require a minimum credit score of 700 for jumbo loans. However, to access the best rates and terms, a score of 760 or higher is ideal. For super-jumbo loans above $2M, which are common in Needham, lenders typically look for 720 to 740.

Are jumbo rates higher than conventional rates right now?

Not necessarily. In mid-2026, jumbo rates for well-qualified borrowers are running very close to, and in some cases slightly below, conforming rates. This is relatively unusual and reflects strong competition among portfolio lenders for high-quality loans. Current mortgage rates show how quickly conditions can shift in the broader market.

How much down payment do I need for a jumbo loan?

The minimum is typically 10%, but putting 20% or more down unlocks better rate tiers and makes your offer more competitive in Needham’s multiple-offer environment. I recommend 20 to 25% whenever possible.

How long does jumbo loan underwriting take?

Jumbo loans involve manual underwriting, which means each file is reviewed individually. Expect the process to take slightly longer than conforming loans, generally 30 to 45 days from application to closing. Having organized documentation ready accelerates this timeline.

Should I consider a 15-year jumbo mortgage for a Needham home purchase?

If you have strong cash flow and plan to stay long-term, absolutely. The 15-year jumbo rate is currently around 5.85% APR, meaningfully lower than the 30-year option. The monthly payment is higher, but the total interest savings are substantial over the life of the loan.

Is a jumbo ARM a good idea in Needham’s market?

For buyers with a defined time horizon of 5 to 7 years, a jumbo ARM at around 6.27% can make financial sense. If you are relocating for a contract position along the Route 128 corridor and know your window, this product deserves a serious look.

What cash reserves do jumbo lenders require?

Most jumbo lenders want to see 6 to 24 months of mortgage payments in liquid, accessible accounts. The exact requirement varies by lender and loan size, which is another reason shopping multiple lenders matters.

Why does my seller care about my jumbo pre-approval?

In Needham, where homes frequently receive multiple offers within the first week, sellers and their agents evaluate not just the offer price but the reliability of the buyer’s financing. A strong jumbo pre-approval from a lender with local experience can be the deciding factor.

How do I find the best Needham Realtor to guide me through jumbo financing?

Look for an agent with deep local market knowledge, a track record of closing high-value transactions, and established relationships with jumbo lenders who operate in MetroWest Boston. Experience matters because jumbo deals have moving parts that standard transactions do not.

The Bottom Line on Jumbo Financing for Needham Buyers and Sellers

The rate environment in 2026 has shifted the conversation from “should I buy in Needham” to “how do I structure this purchase.” Buyers who bought at 3% rates are not selling. That means inventory stays tight, demand stays strong, and the buyers coming into this market need to focus on the asset, the equity build, and their long-term plan rather than trying to time rates.

Whether you are preparing to list a luxury home in Needham or you are a buyer ready to compete, the financing piece is where strategy meets execution. Understanding your loan options is essential before making a commitment. With 26 years of experience in this market and recognition as a Top 1.5% America’s Best Realtor and Boston Magazine Top Real Estate Producer, I have helped clients navigate every rate environment this town has seen. If you have questions about how jumbo rates affect your specific situation, I am always happy to talk. You can reach me, Jane Migdol with Migdol Real Estate LLC at Gibson Sotheby’s International Realty, at (781) 223-5641. My office is right here on Great Plain Avenue in Needham, and I would love to help you make your next move with confidence.

Jane & Jonathan Migdol · Gibson Sotheby's International Realty

Global Real Estate Advisors — MetroWest Boston

Get in touch →